N26 or Revolut? Compare Plans and Perks and See How Zeal Compares

N26 vs Revolut: Complete comparison of banking features, travel perks & costs. See which neobank wins and how Zeal changes the game.

We compared N26, Revolut, and Zeal to help you choose where your money will work hardest. Spoiler: while N26 and Revolut fight over who charges fewer fees, Zeal is asking why you should let banks keep the juicy returns while you get table scraps.

Zeal works differently: it's a non-custodial wallet where you actually own and control your money, not the bank. This lets you access higher yields directly from lending markets.

This breakdown covers 6 key features across all three services, so you'll know exactly which one fits your financial goals and maybe why the old "pick one bank" mentality is fading.

Quick Verdict: At a Glance

| Feature | N26 | Revolut | Zeal |

|---|---|---|---|

| Account Type | 🥇 Full banking | 🥈 Banking + features | 🥉 Card + transfers |

| Card Features | 🥉 Essential features | 🥈 Advanced features | 🥇 High cashback |

| Cost Structure | 🥉 Costly upgrades | 🥈 Good paid value | 🥇 Truly free |

| Global Reach | 🥉 EU-focused | 🥈 120+ countries | 🥇 Worldwide |

| Money Growth | 🥉 Minimal yields | 🥈 Modest returns | 🥇 Real yield |

| Security | 🥇 Deposit insurance | 🥇 Deposit insurance | 🥉 DeFi protocols |

Revolut excels for international power users who want multi-currency accounts, extensive features, and comprehensive travel tools. Best for frequent travelers and digital nomads.

N26 wins for users wanting a clean, bank-like experience with solid insurance options and European deposit protection. Perfect for everyday European banking with occasional travel.

Zeal offers something neither can match: around 3.4% APY on euros PLUS up to 4% cashback on spending. Double money growth while maintaining fee-free global spending. Your money actually working for you instead of the other way around.

What Each Service Won't Tell You

N26 Limitations:

- Low yields: Even premium plans offer low returns on your money

- Limited features: Basic banking without Revolut's bells and whistles

- Foreign ATM costs: Expensive withdrawal fees unless you pay the subscription tax

Revolut Limitations:

- App complexity: Can be overwhelming, like Swiss Army knife syndrome

- FX weekend markups: Higher costs when markets close for the weekend

- Monthly limits: Free plans cap currency exchange at €1,000/month

Zeal Limitations:

- No travel insurance: Unlike N26/Revolut premium plans, offers no coverage for trips

- Limited traditional banking: May not handle all the bureaucracy banks love

- Smart contract risk: Your funds depend on code security, not government promises

- No multi-currency accounts: Unlike Revolut, focuses on EUR/USD rather than currency trading

The reality? Most savvy users combine services. Keep reading to find your perfect setup.

Account Type: Which One Actually Replaces Your Old Bank?

N26: Full Banking Experience

N26 provides comprehensive current account functionality:

- IBAN & Direct Debits: German/French IBAN with full SEPA direct debit support for bills and salaries

- Banking Services: Standard SEPA transfers, account statements, overdrafts (select countries)

- Regulatory Status: Licensed German bank with full deposit protection

- Best For: Users who need complete banking replacement with European focus

Revolut: Banking Plus Multi-Services

Revolut offers current account features plus extensive additional services:

- IBAN & Direct Debits: Lithuanian/French IBAN with SEPA support, though some billers prefer local IBANs

- Banking Services: Multi-currency accounts, international transfers in 25+ currencies, investment tools

- Regulatory Status: Lithuanian banking license with EU deposit protection

- Best For: Users who want banking plus investing, crypto, and international finance tools

Zeal: Self-Custody Card & Transfers

Zeal focuses on earning and spending rather than traditional banking:

- Self-Custody: You own and control your funds directly, no bank middleman

- Core Functions: Card payments globally, basic transfers, high-yield earning

- Regulatory Status: Non-custodial wallet accessing DeFi protocols

- Best For: Users prioritizing yield and global spending over complex banking needs

🥇 Winner: N26 for full banking replacement. Revolut for banking plus financial services. Zeal for simplified earning and spending.

Card Features: Which One Puts More Cash Back in Your Pocket?

N26: Simple and Reliable

- Card Type: Mastercard (virtual card included, €10 for physical card)

- Spending Limits: €1,050 weekly ATM withdrawals, €20,000 monthly spending

- Virtual Cards: Virtual card included with all accounts

- Cashback: 1% on travel spend (limited-time promo), then 1% outside EEA for up to 12 months

- Special Features: Spaces (sub-accounts) for budgeting and savings automation with automated rules

Revolut: Feature-Rich Platform

- Card Type: Visa or Mastercard (free physical card, small shipping fee)

- Spending Limits: Customizable by user (no imposed limits)

- Virtual Cards: Multiple disposable virtual cards, even on free plan

- Cashback: 0.1% in Europe, 1% outside Europe on Metal plan

- Special Features: Multi-currency balances, freeze/unfreeze in real-time

Zeal: The Earning Card

- Card Type: Visa Debit Card via Gnosis Pay (physical card available)

- Spending Limits: Standard Visa limits, customizable in-app

- Virtual Cards: Instant virtual cards for online shopping

- Cashback: Up to 4% (5% for OG NFT holders) paid in GNO tokens

- Special Features: Auto top-up from earning balance, spend your yield directly, Apple Pay support

Real-world example: On €2,000 monthly spending:

- N26: €0 cashback (or €20 during promo periods on eligible travel spend)

- Revolut Metal: €2 cashback (0.1% in Europe)

- Zeal: Up to €80 cashback (4% with GNO tokens, 5% for OG NFT holders)

🥇 Winner: Zeal for actual rewards that matter. Both earning AND spending generate money. Revolut for features and flexibility. N26 for straightforward reliability.

Cost Structure: Who's Really Getting Your Money?

N26: Free Base, Costly Upgrades

- Free Plan: N26 Standard has no monthly fee, but €10 for physical card and 1.7% foreign ATM fees

- Paid Plans: €4.90 (Smart) to €16.90 (Metal) monthly for features many consider basic

- Value Assessment: Premium plans expensive for what they offer; insurance and ATM fee removal cost extra

Revolut: Free with Smart Limitations

- Free Plan: Includes physical card but caps currency exchange at €1,000/month and ATM withdrawals at €200/month

- Paid Plans: €2.99 (Plus) to €45 (Ultra) monthly with substantial feature additions

- Value Assessment: Good value at paid tiers; significant features added for the price

Zeal: No Tiers, No Fees

- Only Plan: €0 monthly, €0 card fees, €0 FX fees ever

- No Limitations: No transaction caps, withdrawal limits, or feature restrictions

- Value Assessment: Everything included from day one, monetization through optional features only

Cost comparison for heavy international user:

- N26 You: €119 annually + ATM fees for unlimited withdrawals and insurance

- Revolut Premium: €120 annually for €400 monthly ATM limit + travel features

- Zeal: €0 fees + €960 annual cashback potential (4% on €2,000 monthly spending)

🥇 Winner: Zeal for pure cost efficiency and earning potential. Revolut for paid tier value. N26 for those who want basic free banking.

International Usage: Where Can You Actually Spend?

N26: European-Focused

- FX Fees: €0 on purchases (all plans)

- ATM Withdrawals: 1.7% fee outside Eurozone (free plans), unlimited free on premium

- Travel Perks: Comprehensive Allianz insurance on You/Metal plans

- Currency Support: Euro-centric, limited multi-currency features

Revolut: The Traveler's Choice

- FX Fees: Near-perfect rates weekdays, markups on weekends

- ATM Withdrawals: €200-€1,200 free monthly depending on plan

- Travel Perks: Airport lounge access, travel insurance on premium plans

- Currency Support: 150+ currencies, real-time exchange, multi-currency accounts

Zeal: Fee-Free Simplicity

- FX Fees: €0 markup on Visa exchange rates, no weekend penalties

- ATM Withdrawals: Standard Visa network access (fees vary by ATM provider)

- Travel Perks: None at the moment (no insurance or lounge access)

- Currency Support: Global Visa acceptance, automatic conversion from earning balance

Real scenario: €5,000 spending in 3 months abroad

- N26 Standard: €0 card fees + ATM withdrawal costs

- Revolut Standard: €20 extra FX fees after €1,000 + weekend markups

- Zeal: €0 fees + potential €200 cashback earnings (4% rate)

🥇 Winner: Revolut for feature-rich travel tools. Zeal for pure cost efficiency. N26 for insurance-backed peace of mind.

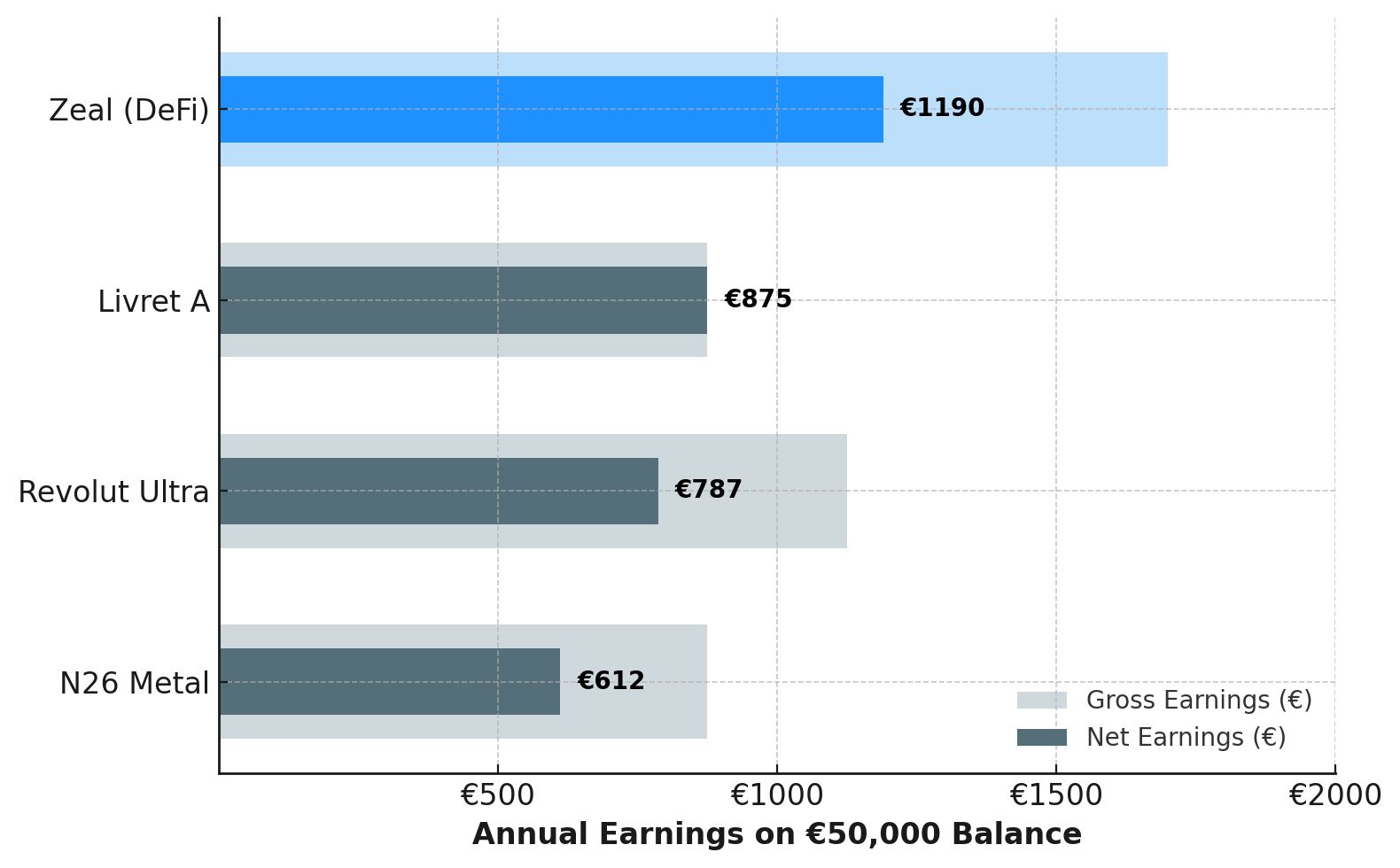

Money Growth: Which Service Actually Grows Your Cash While You Sleep?

The math on €50,000 balance:

- N26 Metal: €875 gross (€612 after tax)

- Revolut Ultra: €1,125 gross (€787 after tax)

- Zeal: €1,700 gross (~€1,190 after tax)

- Livret A: €875 tax-free (but capped at €22,950)

N26: Minimal yields

- Standard Plan: 0.25% APY (a whopping €50 annual on €20,000)

- Premium Plans: Up to 1.75% APY on Metal

- After French taxes: ~1.2% net on the highest tier

- Beats: Your old bank's 0% checking account

- Loses to: France's Livret A at 1.75% tax-free

Revolut: Money Market Approach

- Variable Rates: 1.5%-2.25% APY depending on plan

- Investment Vehicle: Money market funds, not traditional deposits

- Protection: Lithuanian investor protection (€22,000 limit)

- Reality: Revolut keeps ~1% spread from underlying fund performance (classic middleman move)

Zeal: DeFi-Powered Returns

- Current Rate: Around 3.4% APY on euros via Aave protocol

- Compounding: Every second, visible in real-time

- Liquidity: No lock-ups, instant access to funds

- Protection: Over-collateralized lending, not government insurance

🥇 Winner: Zeal by a massive margin. Real money growth vs. symbolic interest rates that barely cover inflation.

Security & Protection: Who's Really Keeping Your Money Safe?

N26: Traditional Banking Safety

- Deposit Insurance: €100,000 per account via German deposit guarantee

- Regulation: Full banking license, BaFin oversight

- Track Record: Established European bank with regulatory backing

- Risk: Minimal for deposits under insurance limit

Revolut: Evolving Protection

- Deposit Insurance: €100,000 per account via Lithuanian banking license (for eligible accounts)

- Regulation: E-money license in most countries, full banking license in Lithuania

- Track Record: Growing pains with compliance, improving over time

- Risk: Low for insured deposits, some concerns about customer service during disputes

Zeal: Code-Based Security

- Deposit Insurance: None - not a traditional bank

- Protection: Smart contract over-collateralization (borrowers must deposit more than they borrow)

- Regulation: Accesses DeFi protocols directly; benefits from Europe's MiCA regulation framework for crypto assets

- Smart Contract Risk: Code vulnerabilities, potential protocol exploits, or technical failures could affect funds

- Risk: Higher reward comes with higher risk (no government guarantees)

Understanding Smart Contract Risk: Unlike traditional banking where your money is "protected" by government insurance (read: taxpayer bailouts), DeFi protocols rely on computer code. While this code is audited and tested, it can still contain bugs or be exploited by hackers. If a smart contract fails, funds can be lost permanently with no government cavalry coming to the rescue.

The philosophical choice: Government promises vs. mathematical guarantees

- Traditional: "If the bank fails, the government will definitely pay you back (trust us)"

- DeFi: "The code ensures borrowers can't access your money without providing more collateral (math doesn't lie)"

🥇 Winner: N26/Revolut for risk-averse users. Zeal for those wanting higher returns with smart contract-based security.

Which Service Fits Your Life?

The Risk-Averse European

Choose: N26 You (€9.90/month) You want solid banking with travel insurance and government guarantees. Perfect for 2-3 international trips yearly with comprehensive coverage.

The International Power User

Choose: Revolut Premium (€9.99/month) You live across borders, trade multiple currencies, and want every financial tool in one app. The subscription pays for itself in convenience.

The Yield Optimizer

Choose: Zeal + Traditional Bank Backup Keep emergency funds in insured accounts, put the rest in Zeal for 3.4% growth PLUS up to 4% cashback on spending. Double your money's productivity with both earning and spending rewards.

The Simple Spender

Choose: Zeal One account, no fees, money grows automatically at 3.4% APY, plus earn up to 4% back on every purchase. Spend anywhere without thinking about exchange rates or monthly charges while maximizing both your savings growth and spending rewards.

The Feature Collector

Choose: Revolut Metal (€16.99/month) You want stock investing, lounge access, and premium everything. You're paying for the full fintech experience.

The Smart Combiner

Choose: Zeal + N26 Standard or Revolut Standard Use Zeal for both earning (3.4% APY) and primary spending (up to 4% cashback). Keep a free backup account for any edge cases or European direct debits. Maximize money growth from both sides of your finances.

The Bottom Line: It's Not Really "N26 ou Revolut" Anymore

The traditional comparison between N26 and Revolut assumes you're choosing between different flavors of the same thing: modern banks that charge slightly less than traditional ones for the privilege of holding your money hostage.

But what if the real question isn't about fees, but about what your money does while it's sitting there earning nothing?

N26 gives you banking reliability with German precision. Revolut offers financial tools with international flair. Zeal asks why your money should earn nothing when it could be growing at 3.4% APY.

The smartest approach isn't picking sides but using the right tool for each job:

- High-yield earning AND cashback rewards: Zeal wins decisively with the double advantage

- Travel insurance and loans: N26 takes this round

- Multi-currency power and features: Revolut dominates

- Pure simplicity and cost: Zeal again

Most financially savvy users are exploring beyond the "one bank for everything" model. Some keep their high-yield savings in newer platforms like Zeal, their travel spending optimized through Revolut or N26, and their emergency funds in whatever offers the best insurance coverage.

The question isn't "N26 ou Revolut?" but rather "How can I make my money work harder while keeping the flexibility I need?"

For many, the answer involves exploring new options: Consider Zeal for both high yield potential AND cashback rewards that compound your money growth from both savings and spending, then add whatever else you need for your specific lifestyle.

Information provided is for educational purposes only and not investment advice. DeFi protocols carry smart contract risks not covered by deposit insurance. Assess your risk tolerance before using any financial service.